Concept of Blockchain Technology and Its Advantages

Introduction

Introduction

Introduction Over the years, ever since the name cryptocurrency has come into notice, the word blockchain along has also come into notice. But beneath the surface, nobody has understood what exactly blockchain is and how it works.

Blockchain is a technology that secures your data or information when sharing. All the data is stored in a database and the transactions are recorded in an account called a ledger. To get in-depth knowledge about blockchain technology and how it works, read the full blog.

Key takeaways

A blockchain is a distributed ledger or database that is shared by all nodes in a computer network.

The blockchain collects data and transacts and transfers it onto a block.

When a block is completed with data, it is linked chronologically to the block before it.

What is Blockchain Technology?

A blockchain is a distributed ledger or database that is shared by all nodes in a computer network. They are mainly known for their vital role in cryptocurrency systems that maintain a secure and decentralized record of transactions, although they have uses beyond cryptocurrencies. Blockchain technology can be used in any business to make data unchangeable, or immutable.

It's a method of recording information that is difficult to hack or steal from the system. A blockchain, also known as a distributed ledger, is a system of interconnected computers that duplicate and distribute transactions among themselves. In simple words, multiple copies are saved on different machines, and they have to match with each other to be valid.

The blockchain collects data and transacts and transfers it onto a block. Once the block is full, the information runs through an encryption algorithm and then it creates a hexadecimal number called a hash. After that, the hash is encrypted along with the other data in the block and added to the next block header. As a result, a chain of linked blocks is produced.

Concept of Blockchain Technology

Imagine buying your favourite moisturiser from an online store, and you track the whole process of packing, shipping, and how long it will take to deliver, what time will it be delivered etc. That is how blockchain technology works. Blockchain helps to record the information transparently at every step. It stores data in blocks that are connected like links in a chain rather than storing it all in one location.

Blockchain is distributed, decentralized, and unchangeable. It is a peer-to-peer ledger that allows data about any event or transaction to be recorded in real-time, and copied across numerous nodes linked to a network. It is recorded as a digital asset using a secure method and is made up of blocks on a chain.

Nowadays when technology is advanced, traditionally recording financial transactions is quite difficult. for example, while buying a property or selling a property, money is exchanged. Now trusting the transaction from both parties is difficult. The seller can easily claim that he hasn't received the money and the buyer can claim of sending the money. This can create a problem, who’s telling the truth?

Here blockchain comes and provides security to your transaction or information. Each block in the chain is linked together and encrypted, which makes it difficult to destroy information. This way it makes the information, transactions and other private information more secure and safe.

A list of the network's transaction history is viewable by anybody with an internet connection on many blockchain networks, which function as public databases. people can view transaction details, but they are not able to access personally identifiable data about the people who are conducting those transactions. There is a popular misconception that blockchain networks, like as Bitcoin, are completely anonymous. In reality, they are pseudonymous, as information may be linked to a user by a visible address.

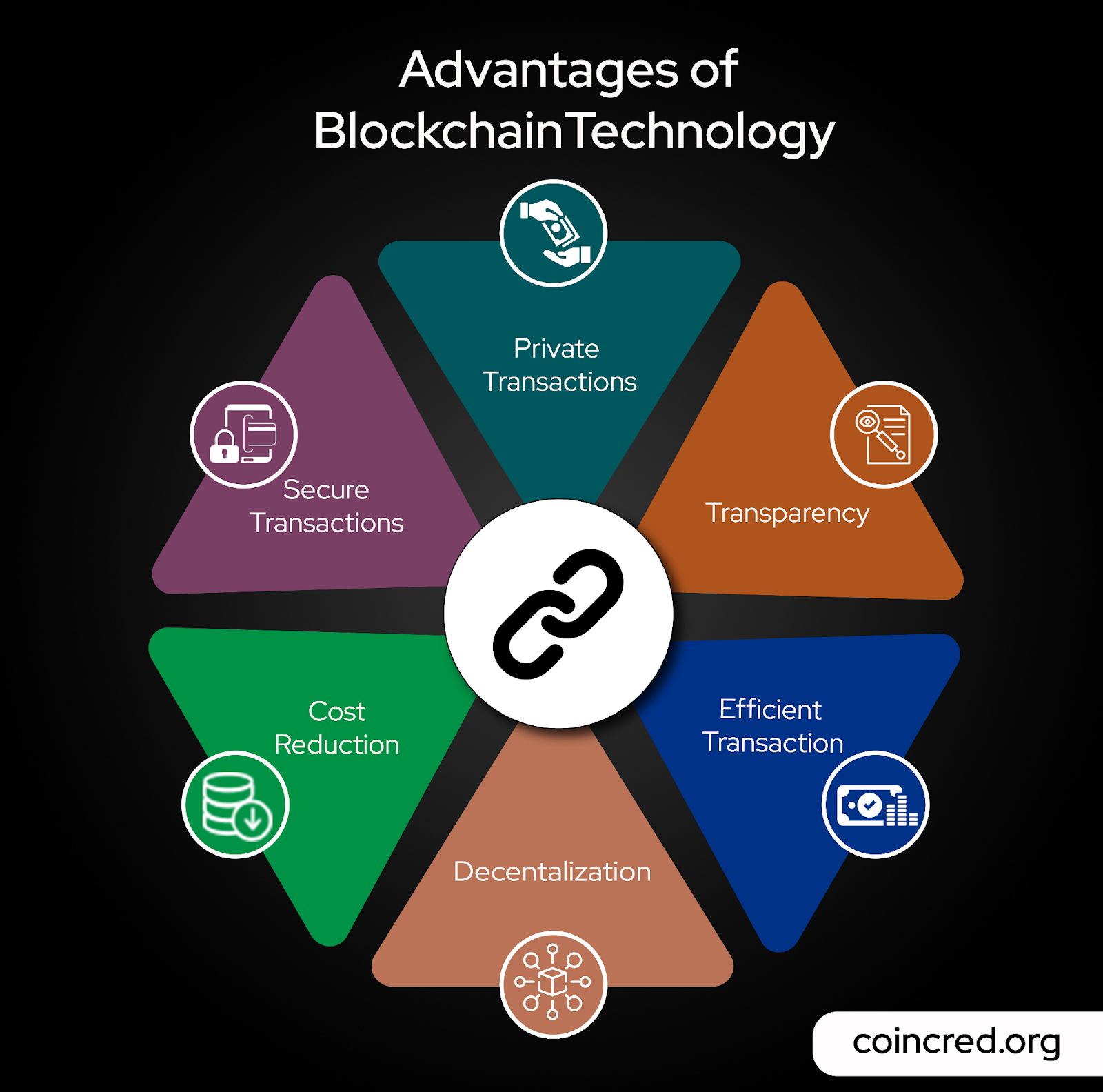

Advantages of Blockchain Technology

Private transactions

Mostly majority of networks are operated as public database. Viewing the transaction history is possible for anyone with an internet connection. However, blockchain technology makes it feasible.

Secure transactions

After every transaction is validated, its added to the blockchain block. Once the transaction is recorded, it’s authenticity is verified by the blockchain network.

Transparency

Transparency is one of the most important components of decentralization. In a decentralized organization, all workers have access to information and decision-making procedures. Employee trust and cooperation are increased as a result of this openness.

Cost Reduction

Customers usually pay a notary to sign a document or a bank to confirm a transaction..Blockchain eliminates the need for third-party verification and the associated costs.

Efficient Transaction

financial institutions are open for business five days a week during these hours, a blockchain is open around-the-clock, 365 days a year.

Decentralisation

Blockchain does not keep any of its data in one single place. Rather, the blockchain is replicated and dispersed throughout a computer network. Every computer connected to the network updates its blockchain to reflect changes made whenever a new block is added to the chain. Blockchain makes it harder to tamper with data by dispersing it over a network as opposed to storing it in a single, central database.

Limitations of Blockchain Technology

Technology cost

Blockchain implementation is very expensive for companies. Most companies are discouraged from implementing this technology due to its capital-intensive nature.

Storage problem

Every piece of data on a blockchain is shared among all of the network's nodes. In this sense, a miner's system's hard drive houses all of the data on a certain blockchain.

Inefficient mining process

Proof-of-Work is a technique used in blockchain mining to produce each block in the network. For each miner to participate in the mining process, they require a powerful computer. Only one miner will receive the block rewards despite several competing to mine a block. A tremendous amount of materials and energy are wasted.

Regulation

There are still restrictions for blockchain in a number of different countries. Furthermore, the usage and implementation of blockchain technology is prohibited by legal requirements in a number of nations and areas.

Conclusion

Blockchain technology is a peer-to-peer distributed ledger that is decentralised, safe, and unchangeable. It is made up of a safe block that is duplicated on several nodes connected to a blockchain network and joined in a chain. Depending on the practical applications of blockchain technology, public, private, and hybrid blockchains can be deployed.

Written by- Manmeet Kaur